Hexicon

0,283

SEK

-5,67 %

Mindre end 1K følgere

HEXI

First North Stockholm

Renewable

Energy

Overview

Finansielt overblik og estimater

Ownership

Investor consensus

-5,67%

+33,49%

+70,07%

+117,02%

+54,31%

-52,44%

-85,85%

-

-90,99%

Hexicon is a project developer in floating wind that opens up new markets in countries with deep water. The company is also a technology supplier with TwinWind, a patented floating wind design. The technology enables increased use of global wind power and can thus contribute to increased access to renewable energy. Hexicon operates in several markets in Europe, Africa, Asia and North America.

Læs mereMarkedsværdi

102,96 mio. SEK

Aktieomsætning

144,63 t SEK

P/E (adj.) (25e)

2,16

EV/EBIT (adj.) (25e)

5,18

P/B (25e)

-0,44

EV/S (25e)

2,91

Udbytteafkast, % (25e)

-

Omsætning og EBIT-margin

Omsætning mio.

EBIT-% (adj.)

EPS og udbytte

EPS (adj.)

Udbytte %

Finanskalender

28.5

2025

Delårsrapport Q1'25

20.8

2025

Delårsrapport Q2'25

19.11

2025

Delårsrapport Q3'25

Risiko

Business risk

Valuation risk

Lav

Høj

Alle

Analyse

Selskabspræsentationer

Selskabsmeddelelser

ViserAlle indholdstyper

Annual general meeting held in Hexicon AB (publ)

Hexicon AB (publ) publishes its annual report for 2024

Join Inderes community

Don't miss out - create an account and get all the possible benefits

Inderes account

Followings and notifications on followed companies

Analyst comments and recommendations

Stock comparison tool & other popular tools

Notice to attend the annual general meeting in Hexicon AB (publ)

Hexicon: A long-awaited divestment, but financing risks persist

Hexicon (publ) Divests two of its Italian Projects to Ingka Investments and Oxan Energy

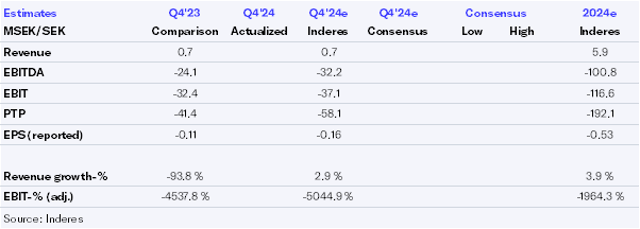

Hexicon Q4'24: Delays in divestments extend funding uncertainty

Hexicon, Webcast, Q4'24

Hexicon AB (publ) releases its interim report for Q4 2024

Hexicon Q4’24 preview: It’s all about divestments

Invitation to the presentation of Hexicon’s year-end report for 2024 on the 19th of February

Hexicon extends its current credit facility

Hexicon extends credit facility

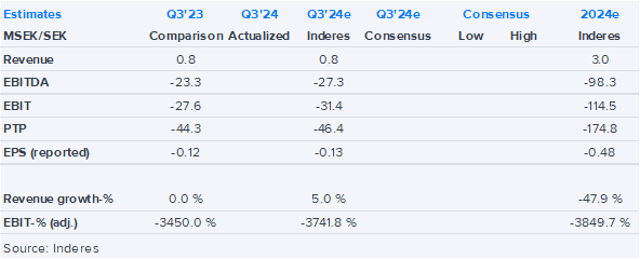

Hexicon Q3'24: Divestments and financing risks still in focus

Hexicon, Webcast, Q3'24

Hexicon AB (publ) - interim report Q3 2024

Hexicon obtains regulatory approval for MunmuBaram

Regulatory Approval Obtained for South Korean Transaction