Metacon is an energy technology company that develops and sells small and large energy systems for the production of hydrogen, electricity and heat. The company was founded in 2011 and has patented technology for the production of hydrogen gas from biogas or other hydrocarbons. The range consists, for example, of gas stations and larger CHP systems. The company has its headquarters in Örebro.

Metacon has announced that the outstanding TO1 warrants have been fully subscribed through a combination of subscription commitments (90.9% of the total outstanding warrants) and guarantee commitments (9.1%). As a result, the company will receive approximately 9.2 MSEK before issuing costs.

Metacon has announced that it is in the final stages of negotiations for an electrolysis-based wind-to-hydrogen production project, valued at 20 MSEK. If the contract is secured, it would support our current estimates. However, it does not immediately trigger any revisions to our estimates or valuation.

Metacon announced that the company has secured full subscription for its outstanding TO1 warrants through a combination of subscription intentions and guarantee commitments. The exercise price for the warrants has been set at SEK 0.09. Given that the current share price is trading significantly above this level, we see a strong likelihood that the warrants will be subscribed without substantial reliance on guarantors. We have already incorporated full warrant subscription at an exercise price of SEK 0.09 into our estimates, so we are not making any adjustments to our estimates or valuation at this time.

With the recent large-scale orders secured, we believe Metacon is better positioned to achieve broader commercialization. That said, we acknowledge the significant risks and uncertainties regarding the company’s ability to consistently secure large orders and maintain sufficient working capital to fulfill them. While liquidity is expected to remain tight until June/July 2025, when we anticipate the release of a significant portion of restricted cash tied to previously announced orders, we believe Metacon is well-positioned to secure short-term project financing on reasonable terms., if needed. With improved near-term revenue visibility, where our 2025 revenue estimates are largely backed by the existing order book, we believe the current valuation offers an attractive risk/reward profile. As a result, we reiterate our Accumulate recommendation with an increased target price of SEK 0.16 (was SEK 0.12), mainly due to an upward revision of our estimates.

Metacon announced that it has signed a supplementary agreement with PERIC, granting Metacon the rights to manufacture the central modules in electrolysis systems. In our view, if manufacturing and sales prove successful, this could help establish a more stable, long-term revenue stream beyond the one-off sales of new electrolysis systems. However, while the supplementary agreement supports the foundation of our estimates, it does not necessitate immediate revisions.

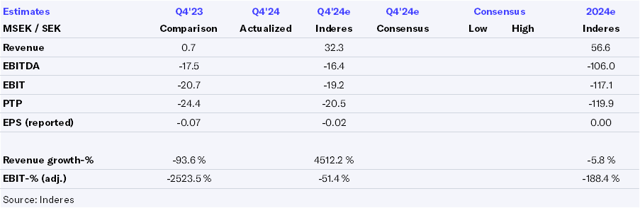

Metacon’s Q4 report fell below our expectations, with lower-than-expected revenue recognition from the Motor Oil order and higher fixed costs. We acknowledge the significant risks and uncertainties surrounding Metacon’s ability to consistently secure large-scale orders and maintain sufficient working capital to fulfill them. However, at this stage, we believe the company is well-positioned to obtain additional short-term funding, if needed, on reasonable terms. With increased near-term revenue visibility, where our 2025 revenue estimates are largely covered by the existing order book, we believe the recent drop in valuation presents an attractive entry point. While we maintain our target price of SEK 0.12 per share, which is at the lower end of our acceptable valuation range, the current valuation offers an attractive risk/reward profile, as the share price has fallen by around -23% and the expected return exceeds our required return. Consequently, we raise our recommendation to Accumulate (previously Reduce).

Metacon will release its Q4 results on Wednesday. We anticipate a significant increase in revenue, primarily driven by the expected recognition of revenue from the large-scale order from Motor Oil. However, given the variable nature of raw material and consumable costs, which are expected to scale up with revenue, we believe EBIT will remain negative. In the upcoming report, we look for management’s comments on the demand situation and further insights into the company’s financial position.

Metacon has announced that it has acquired additional shares in Pherousa, a Norwegian technology transfer company within the maritime industry, bringing its total ownership to 35% of the capital. With this increased shareholding, along with an updated exclusive license agreement, we believe that Metacon is gaining a larger stake in an innovative company in an exciting market at a seemingly low cost. However, this news does not directly impact our forecasts or our view on the stock.

We have received some investor questions regarding our net liquidity calculation for Metacon's recent rights issue, as presented in our latest research update. This note clarifies those details.

As noted in our recent research report, 41 MSEK is our estimate of the net new funding coming in at the conclusion of the rights issue after the company repaid its bridge loan and related costs. To clarify, this comes on top of the 50 MSEK bridge loan taken earlier at the beginning of the rights issue. In total, we estimate the company to have secured 91 MSEK new funding in Q4’24.

As detailed in our report, we estimate that the current funding will last until around summer 2025, based on a quarterly burn rate of 25–30 MSEK. We also anticipate that approximately 180–190 MSEK from the Motor Oil order will be released around the same time. This means that the liquidity situation is tight and that the burn rate over the coming quarters and the timing of when liquidity from the project is released will significantly influence whether the company will need to secure additional financing before generating positive cash flows from the Motor Oil order. Regardless of the timing, based on our current estimates outlined in the recent research report, we believe that Metacon will require additional financing during the next 2–3 years before reaching cash flow neutrality, unless new customer projects require less working capital during the initial phase. We are particularly interested in more details regarding the timing of cash flows from the Motor Oil order, the current burn rate, and Metacon’s financial position in its Q4’24 report, which will be released on February 26.

Inderes uses cookies to provide a better user experience and a personalised service. By consenting to the use of cookies, we can develop an even better service and will be able to provide content that is interesting to you.