Vincit

1,655

EUR

0 %

8.081 følger denne virksomhed

VINCIT

First North Finland

Software

Technology

Overview

Finansielt overblik og estimater

Investor consensus

0%

-8,06%

-4,06%

-3,78%

-19,27%

-38,93%

-70,91%

-60,6%

-72,87%

Vincit provides services in design and software development. The services include, for example, software for e-commerce and web applications, cloud platforms, mobile applications and IoT solutions. The services are used by both small and medium-sized corporate customers. The main operations are in Europe and North America. Vincit was founded in 2007 and is headquartered in Finland.

Læs mereMarkedsværdi

28,06 mio. EUR

Aktieomsætning

45,77 t EUR

P/E (adj.) (25e)

14,11

EV/EBIT (adj.) (25e)

7,47

EV/S (25e)

0,25

Udbytteafkast, % (25e)

7,25 %

Omsætning og EBIT-margin

Omsætning mio.

EBIT-% (adj.)

EPS og udbytte

EPS (adj.)

Udbytte %

Finanskalender

17.7

2025

Delårsrapport Q2'25

23.10

2025

Delårsrapport Q3'25

Risiko

Business risk

Valuation risk

Lav

Høj

Alle

Analyse

Selskabsmeddelelser

ViserAlle indholdstyper

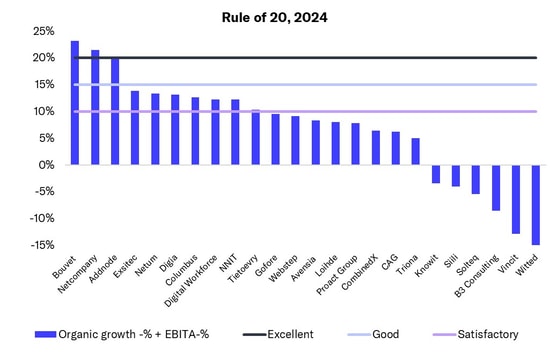

In the IT service sector, a few Nordic companies achieved excellent performance measured by the 'Rule of 20'

IT service sector: Q4 was tough, as was 2024

Join Inderes community

Don't miss out - create an account and get all the possible benefits

Inderes account

Followings and notifications on followed companies

Analyst comments and recommendations

Stock comparison tool & other popular tools

Introducing the Rule of 20: The best measure for IT services performance signals market softening

IT service sector: Bottom of cycle passed, grain will be separated from chaff in 2025

Q3 IT service sector summary: Revenue down but profitability up – sector shows clear divide

IT service sector: Market performance in Denmark and Norway better than in Finland and Sweden

IT services sector 2024 expectations fell slightly in Q2, but H2 looks a little better

Q2 IT service sector summary: Slightly steeper revenue decline, improved profitability and signs of demand bottoming out

IT services sector's 2024 expectations fell slightly in Q1 - revenue expected to remain flat and profitability to rise slightly

IT service sector Q1 summary: Revenue and profitability down from a strong comparison period, but some defensive wins in profitability as well

IT service sector: Our expectations for 2024 generally at the lower end of companies' guidance

Q4 IT service sector summary: Growth and profitability in line with our expectations, 2023 can be seen as a defensive win

IT service sector valuation levels at the bottom of our 7-year monitoring history, justifiably?

We expect the IT services sector to grow moderately and profitability to increase slightly in 2024

IT services sector Q3 summary: Better than feared with several areas continuing to perform well