Witted Megacorp

1,29

EUR

+7,5 %

1.477 følger denne virksomhed

WITTED

First North Finland

IT Services

Technology

Overview

Finansielt overblik og estimater

Investor consensus

+7,5%

-6,52%

-18,35%

-14%

-21,82%

-34,02%

-

-

-73,93%

Witted Megacorp is an IT company. The company offers a wide range of consulting services and IT solutions, mainly services related to project and business development. The solutions are used by a number of corporate customers in various sectors. In addition to the main business, various services are offered. The largest business operations are in the Nordic market.

Læs mereMarkedsværdi

19,95 mio. EUR

Aktieomsætning

49,92 t EUR

P/E (adj.) (25e)

17,29

EV/EBIT (adj.) (25e)

9,47

EV/S (25e)

0,22

Udbytteafkast, % (25e)

1,55 %

Coverage

Omsætning og EBIT-margin

Omsætning mio.

EBIT-% (adj.)

EPS og udbytte

EPS (adj.)

Udbytte %

Finanskalender

23.4

2025

Selskabsgennemgang Q1'25

29.4

2025

Generalforsamling '25

30.4

2025

Årligt udbytte

Risiko

Business risk

Valuation risk

Lav

Høj

Alle

Analyse

Selskabsmeddelelser

ViserAlle indholdstyper

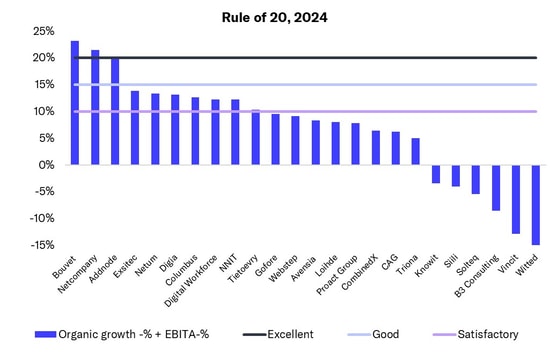

In the IT service sector, a few Nordic companies achieved excellent performance measured by the 'Rule of 20'

IT service sector: Q4 was tough, as was 2024

Join Inderes community

Don't miss out - create an account and get all the possible benefits

Inderes account

Followings and notifications on followed companies

Analyst comments and recommendations

Stock comparison tool & other popular tools

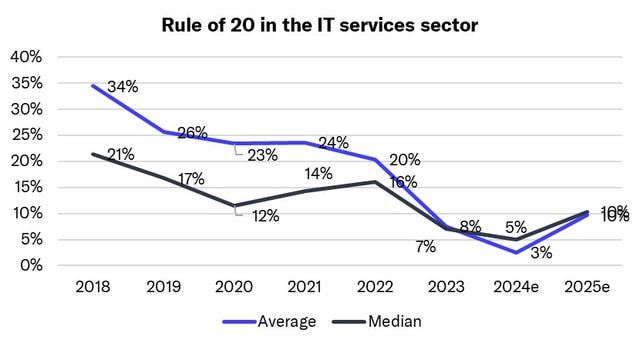

Introducing the Rule of 20: The best measure for IT services performance signals market softening

IT service sector: Bottom of cycle passed, grain will be separated from chaff in 2025

Q3 IT service sector summary: Revenue down but profitability up – sector shows clear divide

IT service sector: Market performance in Denmark and Norway better than in Finland and Sweden

IT services sector 2024 expectations fell slightly in Q2, but H2 looks a little better

Q2 IT service sector summary: Slightly steeper revenue decline, improved profitability and signs of demand bottoming out

IT services sector's 2024 expectations fell slightly in Q1 - revenue expected to remain flat and profitability to rise slightly

IT service sector Q1 summary: Revenue and profitability down from a strong comparison period, but some defensive wins in profitability as well

IT service sector: Our expectations for 2024 generally at the lower end of companies' guidance

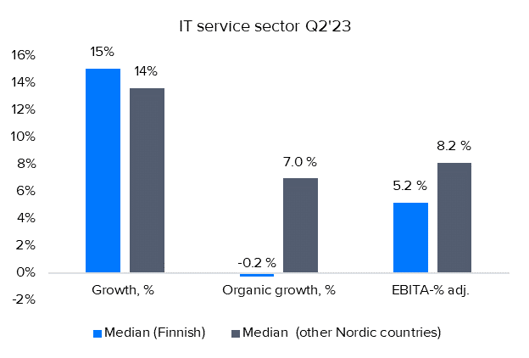

Q4 IT service sector summary: Growth and profitability in line with our expectations, 2023 can be seen as a defensive win

IT service sector valuation levels at the bottom of our 7-year monitoring history, justifiably?

We expect the IT services sector to grow moderately and profitability to increase slightly in 2024

IT services sector Q3 summary: Better than feared with several areas continuing to perform well