B3 Consulting Group operates in the consulting industry and focuses on business and IT strategies, change management and digital transformation. The company's services are aimed at companies and organizations that need support in development projects. The operations are primarily concentrated in Sweden, with a main presence in the Stockholm region. B3 Consulting Group was founded in 2001 and is headquartered in Stockholm, Sweden.

Minor, positive estimate revisions Stable utilisation rate and positive margin surprise '25e EV/EBITA of ~8x, FVR reiterated Improving conditions allow for pos. net recruitment in H2'25 Q1 missed slightly on sales but beat on adj. EBITA compared with...

Sales -3% vs. cons, adj. EBITA +21% vs. cons Announces growth initiatives & cost savings efforts Consensus EBITA estimates likely up by low single-digits Q1'25 report Q1 was slightly softer than expected with respect to sales but better with respect ...

We cut '25e-'27e adj. EBITA by 13-1% Gross profit per consultant at normal levels in '26e '25e EV/EBITA of 7.5x What to expect in Q1'25e We expect sales of SEK 335m for Q1'25e, implying y-o-y growth of 19% (of which the organic decline is -5%), along...

Join Inderes community

Don't miss out - create an account and get all the possible benefits

Inderes account

Followings and notifications on followed companies

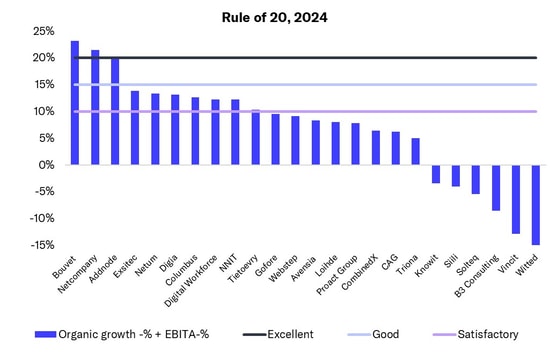

We examined Nordic, listed IT service companies with the 'Rule of 20' metric we launched, measured with which a few companies achieved excellent performance in 2024. On average, Finnish IT service companies fared worse last year than other Nordic companies. Overall, however, it can be said that 2024 was still challenging throughout the Nordics.

Minor estimate revisions due to M&A contribution Utilisation trend is positive '25e EV/EBITA of 8x, FVR reiterated The utilisation is coming back Q4 missed slightly on sales and adj. EBITA compared with consensus' expectations. Organically, sales declined...

Sales -5% vs. cons, adj. EBITA -33% vs. cons Enters Norway with Habberstad acquisition Acquisition offsets negative consensus estimate revisions Q4'24 report Q4 was softer than expected. B3 generated net sales of SEK 336m (-5% vs. FactSet cons, -5% vs...

We cut '25e-'26e adj. EBITA by 10-1% Utilisation should pick up in H2'25e '25e EV/EBITA of ~8x What to expect in Q4'24e We expect sales of SEK 354m for Q4'24e, implying y-o-y growth of 21% (org. -5%, M&A +25%, FX +0.4%), along with EBITA of ~SEK 23m,...

- Minor estimate revisions - Decline in utilisation appears to have stopped - '25e EV/EBITA of 8x H2 increasingly likely to mark a trough Although Q3 was tough for B3, the company performed slightly above expectations. Sales declined organically by ~...

Sales +4% vs. cons, adj. EBITA +20% vs. cons Minor positive consensus estimate revisions Awaiting improving market conditions Q3'24 report Q3 was slightly better than expected. B3 generated net sales of SEK 245m (+4% vs. FactSet cons, +4% vs. ABGSCe)...

We cut '24e-'26e EBITA by 21-4%... ...due to weaker IT consulting market data '25e EV/EBITA of ~7x What to expect in Q3'24e We expect sales of SEK 236m for Q3'24, implying y-o-y growth of ~6% (org. -10%, M&A +15%), along with EBITA of SEK ~5m, corresponding...

- '24e-'26e adj. EBITA down 3-2% - Increasingly likely that Q3'24 will be the trough - NTM EV/EBITA of ~8x Q4 could be a turning point Q2 was another challenging quarter for B3, with sales and EBITA declining by 11% and 61% y-o-y, respectively. Compared...

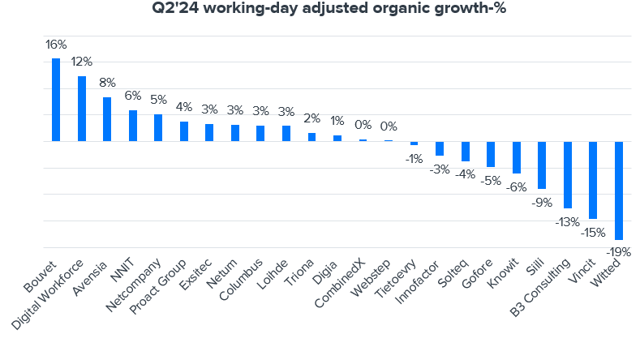

- Sales -2% vs. cons, adj. EBIT -19% vs. cons - Utilisation up due to reduction of unstaffed FTEs - Possible demand recovery in Q4 Q2'24 report Q2 was another challenging quarter with dropping utilisation y-o-y and negative net recruitment. B3 generated...

What to expect in Q2'24 We expect sales of SEK 266m for Q2'24, implying a y-o-y decline of -11%, along with EBITA of SEK ~9m, corresponding to an EBITA margin of 3.3%. Our new estimates mean that we have reduced Q2 sales and EBITA by 2% and 20%, respectively...

SEK 100m run-rate sales contribution excl. sub-contractors Potential to earn 8-9% EBIT margin Acquired at ~4x EV/EBIT on potential earnings Acquires Webstep AB at seemingly trough earnings B3 has announced that it will acquire Webstep's Swedish subsidiary...

We lower '24e-'26e adj. EBITA by 35-1% Potential for utilisation improvement in H2'24 '24e-'25e EV/EBITA of 12-6x It's still tough out there Q1 was undoubtedly a tough quarter for B3, and seemingly also for other IT consulting businesses. B3's sales ...

Sales -6% vs. cons, adj. EBIT -18% vs. cons Drop in utilisation lowered sales by ~9% y-o-y alone Margins prioritised over growth Q1'24 report Q1 was a tough quarter as utilisation was low and net recruitment was negative. B3 generated Q1'24 net sales...

We lower '24e-'26e adj. EBITA by 10-3%... ...on continued weakness in macro data '24e EV/EBITA of ~8.5x What to expect in Q1'24 For Q1'24, we expect sales of SEK 293m, implying a y-o-y decline of -10%, along with an EBITA of SEK 17m, corresponding to...

We lower '24e and '25e adj. EBITA by 3% and 6% 5% EBITA growth in '24e driven by HQ cost cuts '24e EV/EBITA of ~8x Little can be done to combat a weak market Q4 was a tough quarter for IT consulting businesses. B3's sales declined by nearly 12%, whereas...

Sales -3% vs. ABGSCe, adj. EBIT -28% vs. ABGSCe Drop in utilisation lowered sales by ~8% y-o-y alone Proactive in stopping underperforming start-ups Q4'23 report B3 generated Q4'23 net sales of SEK 294m (-3% vs. ABGSCe 302m) and adj. EBIT SEK ~17m (-...